17 Jul 2023

Will inheritance tax increase under Labour – or be abolished by the Conservatives?

The abolition of inheritance tax is reportedly being considered as a possible Conservative manifesto commitment at the next general election, according to The Sunday Times on 16 July. The issue has been the subject of renewed debate since at least 1 June, when The Daily Telegraph splashed on calls from more than 50 Tory MPs for Rishi Sunak to scrap the “morally wrong” tax on account of its perceived unfairness.

The front page of tomorrow’s Daily Telegraph:

Scrap unfair inheritance tax, MPs tell Sunak#TomorrowsPapersToday

Sign up for the Front Page newsletterhttps://t.co/x8AV4OoUh6 pic.twitter.com/vvT28SKg6Z

— The Telegraph (@Telegraph) May 31, 2023

There is plenty of politics at work here, but our interest is as tax advisers and the outlook for a tax that has been with us, one way or another, for hundreds of years and is forecast to raise £7.2 billion in 2023/24.

Is inheritance tax unfair?

Those claiming that the tax burden is unfairly shared have a point.

Cutting inheritance tax has previously been done in the form of reducing the main rate, increasing nil rate bands (effectively the threshold at which it starts to be paid) and introducing exemptions, such as within marriage, for charities and business and agricultural reliefs. So, there are various ways that the burden of inheritance tax can be changed.

A separate issue is that the burden of inheritance tax is not equally borne by estates. Using 2016/17 figures, broadly the effective tax rate increases up to an estate value of about £3 million, then more or less plateaus up to estates of around £9 million, and then falls sharply – principally because of reliefs. So, those claiming that the tax burden is unfairly shared have a point. A good analysis of the way the tax works, and potential changes that could be made, was issued by the Office for Tax Simplification (OTS) on 5 July 2019 – ‘Inheritance Tax review: Simplifying the design of the tax’.

Is inheritance tax likely to increase?

It is very difficult for a government to reduce inheritance tax at a time when its finances are deteriorating.

My colleague Hannah Boniface and I have been considering whether there is a correlation between death duties and the state of the economy, as a possible guide to the future. My recollection is that death duties were higher when we have had very high government debt and were only reduced when the economy was improving, or more particularly, when government debt had been reducing.

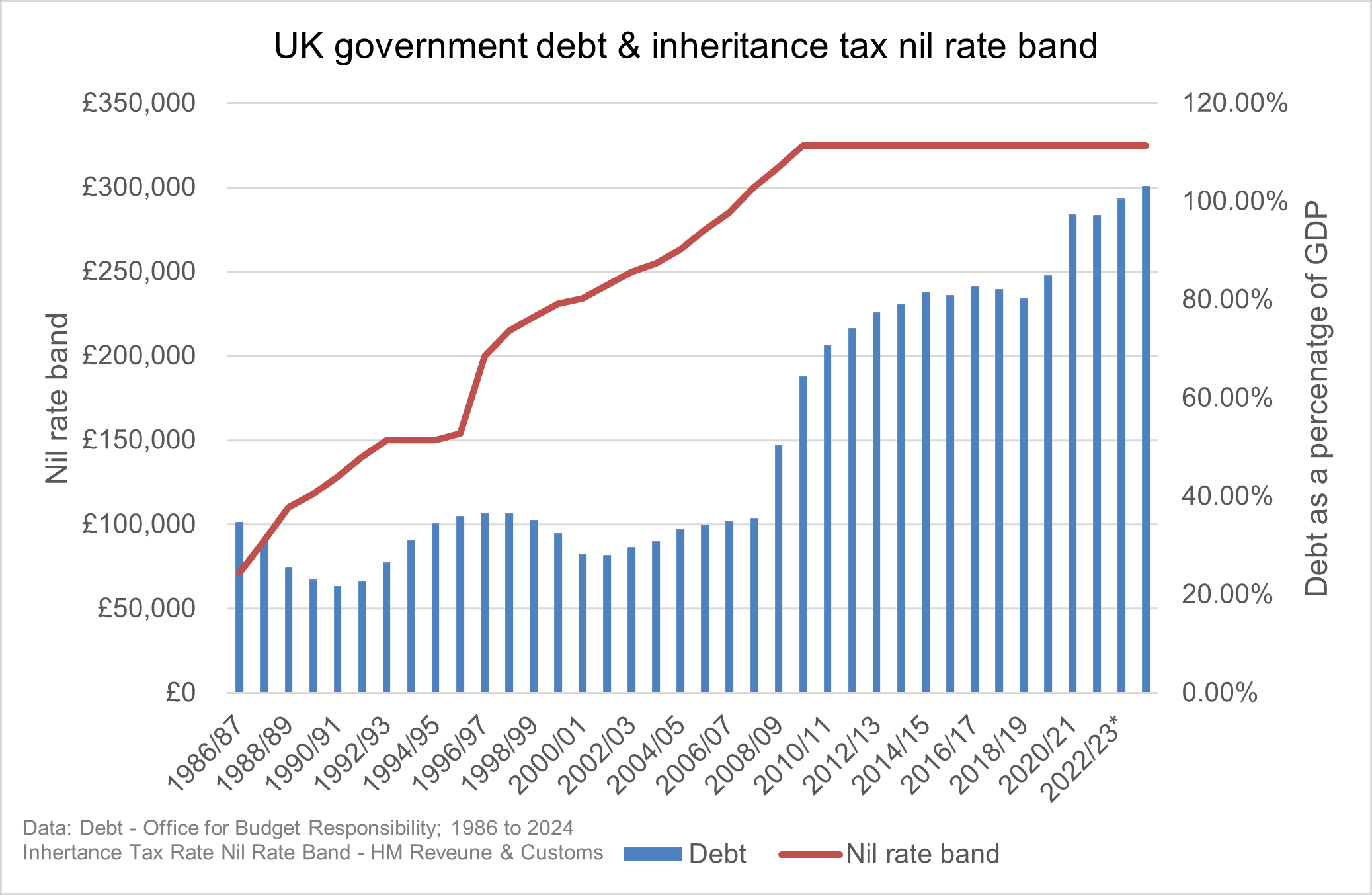

One way of assessing this is to look at the level of the nil rate band since inheritance tax was introduced in 1986 and to compare that against government debt as a percentage of gross domestic product (GDP) over the same time period. This is set out in the graph below.

When the nil rate band was increasing between 1986 and the financial crash in 2008 then at the time, debt as a proportion of GDP was roughly staying at around 40% across that 22-year period. Since 2008, government debt has increased from 40% to 100% of GDP and at the same time the nil rate band has remained the same. That does suggest that it is very difficult for a government to reduce inheritance tax at a time when its finances are deteriorating. This leads us not to expect a significant increase in the nil rate band any time soon.

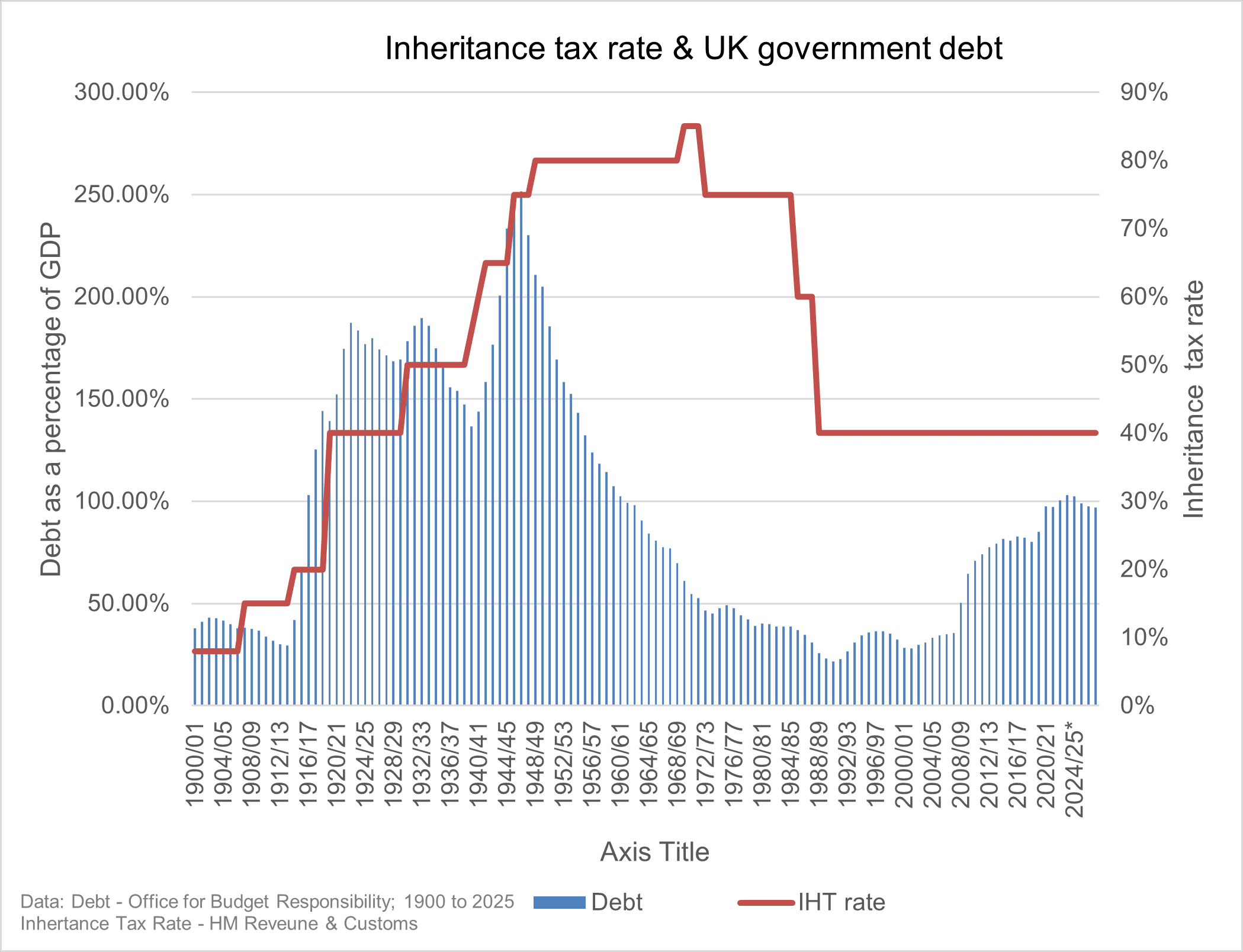

Our second graph, below, shows the top rate of tax alongside debt as percentage of GDP, since death duties were reformed in 1894.

From 1900 to the Second World War, the rate of tax increased more or less in line with government debt as a percentage of GDP, from less than 10% to 80% by the 1940s. Post-war, the position is less clear cut but broadly the tax rate remained somewhere around 80% until the late 1960s and then started to reduce during the 1970s, with the very big reduction to 40% in the mid-1980s – where it has remained ever since.

This rate of 40% still looks consistent with the current level of government debt, but should debt increase much more as a percentage of GDP then it seems likely that the tax rate would increase. The logic being that as most of the taxes would already have reached their maximum limits, then more tax on wealth seems to be the only place to go. There is a limit to how effective wealth taxes can be because the tax is on illiquid assets, but on death, forcing assets to be sold is more acceptable.

On 13 July, the Office for Budget Responsibility (OBR) suggested, in its ‘Fiscal risks and sustainability’ report, that government debt as proportion of GDP might reach 310% by 2070. If so, then the outlook for the top rate of tax is more likely to be up than down.

It seems much more likely that inheritance tax may instead increase in some form.

Could inheritance tax be made fairer?

My assessment is that inheritance tax isn’t going away any time soon. If it isn’t, then could it at least be made more progressive?

One recent report was ‘How to match higher taxes with better taxes’ by the Resolution Foundation (28 June 2023). This is a document likely to find favour with the Labour Party. It includes a chapter on “Taxing pensions and inheritances more consistently”. The ideas include:

- Imposing capital gains tax on death

- Either removing or restricting business and agricultural reliefs

- Abolishing the residence nil rate band

- Reducing the tax rate on lower value estates (20% on estates up to £1 million and 30% up to £1.5 million)

Given the latest opinion polls suggest that Labour is likely to form the next government and the general election is going to have to occur within the next 18 months, then the abolition of inheritance tax seems highly unlikely. It seems much more likely that inheritance tax may instead increase in some form under a new government, although it is hard to generalise. Higher tax is more likely to fall on much larger estates, or on those estates that currently qualify for business and agricultural reliefs.

Find out more about PKF Francis Clark’s inheritance tax specialists.

Written by

Related insights